The 2 Best Leveraged ETFs And How To Use Them

Why do novices lose money with leveraged ETFs?

Leveraged ETFs are a double-edged sword. You can seriously damage your portfolio if you don't know how to use them. However, if you know how to do it, it is an excellent way to reduce risk and increase the profitability of your portfolio.

Today I will give you a series of tips that, as an individual investor, you should take into account if you want to use them correctly. I will also show you the most significant risk you are exposed to, but I will tell you in advance that it is to lose all your investment.

Let's start. Leveraged ETFs are the first instrument that novice investors turn to when they go to the stock market. They have read some finance books and are convinced that indexing is the best alternative. The market has historically given 6% returns, so if I buy a leveraged ETF and hold it for 30 years, I will get a 12-18% annualized return. WRONG!.

If your head is that simple and you still think so, I am going to explain with a table why this is not really so.

If your ETF drops 80%, you need a 400% return in order to get back to where you were initially.

The biggest market declines historically have been:

This implies that in the last 40 years, we have had six declines (2020 is not included in the chart) greater than 20%. This implies a fall in a leveraged ETF (x3) of 60%.

In the case of a normal ETF, it needs a 25% rise from the low to be able to return to the highs. However, a leveraged ETF needs a 150%, or in other words, a 50% rise in the markets.

I think you are beginning to understand why, if not used correctly, it can pose a great risk to your portfolio. If, on the other hand, we expose ourselves to 2008, our leveraged ETF would decline by 99.9999%, and it would be totally impossible to recover.

Volatility

What we have just told you so far is only half true because we have not taken volatility into account.

During a bear, market volatility becomes higher. Generally, the biggest market rallies occur during bear markets, which means that volatility increases.

The chart below shows that the more volatility increases, the more losses increase during a bear market.

When the index's volatility exceeds certain levels, the probability of losing money increases.

Time

To these variables we have above, we must add time. The longer the time frame, the greater the difference between the two returns. In bull markets, despite having a positive return in all time periods, at three years, the return of the Leveraged ETF is (much) higher than the normal ETF and at various times differs greatly from the theoretical double (or triple) that could be expected. Therefore, we must be clear that if we invest in these products at longer maturities, there can be large differences between the two returns, with the performance of the Leveraged ETF becoming negative despite the positive performance of the index.

Now that you know the implications, here are our two favorite leveraged ETFs:

UPRO

UPRO seeks daily investment returns, before fees and expenses, that are three times the return of the S&P 500 index for a single day, measured from one net asset value (NAV) calculation to the next.

The fund's leverage is reset daily, implying that it is three times what the S&P 500 has done at the end of each day.

It is one of the best alternatives for an asymmetric portfolio.

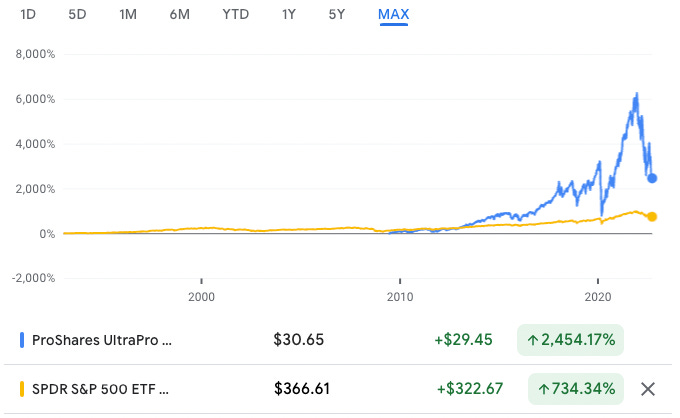

Even after such a radical decline in the indexes from highs, we see that since 2009 this index has more than beaten the S&P 500.

In fact, the SPY (yellow line) in 2009, which is when UPRO begins, has a cumulative return of 100%.

Surprisingly, before the falls, the return was 6,000%. We sold a portion of our position then, and we increased our position throughout the fall.

ProShares Ultra MidCap400

Our second leveraged ETF focuses on U.S. mid-cap stocks. The objective of the ProShares Ultra MidCap400 is to achieve a daily return that is twice that of the S&P Midcap 400 Index, the underlying benchmark. The fund went public in August 2006 and has about $187.5 million under management.

MVV's top holdings include Signature Bank, which accepts Bitcoin; managed healthcare services provider Molina Healthcare. FactSet (NYSE:FDS) Research Systems, which provides financial information and analysis; real estate investment trust (REIT) Camden Property Trust, Builders FirstSource, which supplies building materials; and Trex Company, which manufactures composite decking.

Now let's compare it against the same ETF without leverage:

You can't see it, but today's performance from August 2006, before the great recession, is only slightly higher for the leveraged ETF (253.4%) than for the unleveraged ETF (211%).

So why do we like this ETF? Because it shows us that Leveraged ETFs only make sense with large-cap companies. That we should know what we are doing and be very careful where we put our money.

How to use these ETFs.

As we have said before, these ETFs cannot be bought as a single asset in a portfolio. They have to be part of an asymmetric portfolio. This way, when some assets go down, others go up, and we benefit from all market situations.