Weekly Paid Newsletter 11/21/2021

Managing Volatility Like a Sniper. Asymmetric Portfolio +23.94% YTD.

📚 The best library is just a click away!

The library that we would have liked to have been recommended at the beginning, we make available to our subscribers.

Every 1-2 weeks we will add a book or a summary to this library. All the books are real gems, we promise you, and for only $5/month or $30/year. Between you and me, it's a gift.

What will we talk about? A little bit of everything: finance for beginners, advanced finance, behavioural economics, macroeconomics, how to start an online business, and even soft skills to be a better speaker and get a 'yes' in any conversation.

As long as you take 1% of each of them and put them into practice, you will go a long way.

This week we'll share with you a basic one for those of you just starting out, it won't teach you how to be rich, but it will help you start to change your mindset.

"Rich Dad, Poor Dad".

Managing Volatility Like A Sniper

If you have been with us for a long time, you will know that we are Contrarian investment lovers. We are not in a hurry to reach our goal, knowing that no matter what happens we will get there.

Along the way, we are learning, enjoying day by day the pleasures of life and we do not waste half a minute in analyzing companies because we have a faithful friend called MSCI World that is in charge of choosing them for us. In 10 years, only 10% of active managers beat it; in 20 years, 3%; and in 30 years, 0.01%. Are you going to be one of them?

But what does this have to do with the sniper? The best way to do this is to tell a story.

Maybe many of you know him, his name is Chris Kyle, and he was the most lethal sniper in the US Army. The Pentagon credits Chris with 150 kills, although in his book he puts it at 250, one of them almost 2km away. This has made him the most lethal US sniper ahead of Adelbert Waldron, with 109 kills in Vietnam.

After serving his country four consecutive tours of duty in the Iraq war as a member of the elite Navy Seals. Kyle was unexpectedly shot and killed by a reserve Marine this weekend at a Texas firing range.

Kyle was capable of spending up to 12 hours at a time concentrated in a guard position, waiting to pull the trigger. He is aware that his chance of being shot down is practically null. He was in a totally convex position. Limited losses and unlimited gains.

However, the rest of the combatants are in a totally concave position, with unlimited losses and limited gains.

At Asymmetric Finance, we manage volatility, among other assets, in the same way. Without haste, waiting to pull the trigger, knowing that sooner or later we will be with the target in sight. Specifically every 3.5 years on average.

Volatility is capable of being flat for years and in just a few days jump +300% and with the VIX above 40, fundamentals cease to matter and it is almost an obligation to have a part of it in the portfolio:

Correlation begins to polarize:

When volatility rises the correlation between assets begins to increase. This means that when one falls, they all fall. This is basically what Lynch considers "diworsification".

Volatility hedging is a necessity, not a luxury:

Any car or homeowner will attest that the benefit of having an adequate amount of catastrophe insurance is financial survival. When applied to investing, there is also a secondary benefit.

Thus, "tail hedging" is a long-term offensive strategy, even if it comes at a cost.

Volatility creates "non-linear and explosive" liquidity.

Volatility creates "non-linear and explosive" liquidity when liquidity is difficult to obtain. It allows the portfolio to be positioned more efficiently both ex-post and ex-ante. While it is obvious that explicit tail hedges allow one to have defence in the portfolio, i.e., protect the portfolio from permanent losses, it is also important to note that having tail hedges in the portfolio allows one to hold positions during periods of volatility that can subsequently lead to longer-term gains.

Spikes in the VIX force forced sales.

It is when market turbulence occurs that forced selling occurs. Spreads in portfolios jump and investors are forced to sell their positions at a discount.

Currently, the markets are at all-time highs in leverage and this will mean that when the market explodes it will take a lot of people down with it.

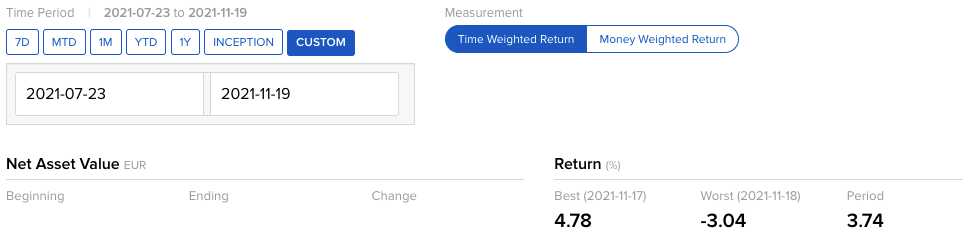

Imagine our portfolio in extreme situations

This week a very curious event took place: during the 17th and 18th sessions, our portfolio registered the highest rises and falls since July (+4.78% and -3.04%, respectively).

This occurred because the IV (the factor that very few know and do not know how to use) rose slightly for very OTM strikes.

Imagine if with that IV rise there was a rise in the portfolio of almost 5%, what can happen in extreme situations...

Below, our portfolio in detail…