I Sold Almost All My Equities. And I Don't Regret It.

Japan 1989. Nasdaq 2000. Are You Sure This Time Is Different?

There are moments when the market speaks to you clearly. Not through a data point. Not through a headline. Through a visceral feeling, built over months of observation, that tells you: something doesn’t add up.

I’ve had that feeling for weeks. And recently, I acted on it.

I reduced my equity exposure to practically zero. I moved roughly 70% of my portfolio into cash and cash equivalents. Not as a temporary refuge. As a strategic position. Because I believe what’s coming isn’t a correction. It’s a structural reset that most investors haven’t processed yet.

Before I get into what I’m doing and why, I want us to look back. Because history has a very unpleasant way of repeating itself for those who don’t study it.

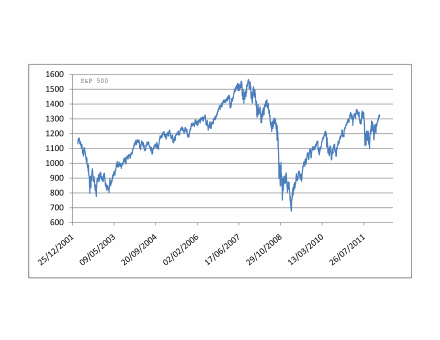

In 2000, the Nasdaq traded at 80 times earnings. Market consensus was that the internet had changed everything, that traditional valuation rules no longer applied, that anyone not invested was an idiot. Pension funds piled into tech. Retail investors sold homes to buy stocks. FOMO was the dominant investment strategy.

The index took more than twelve years to recover its highs. Twelve years. A generation of savings destroyed, not by an unpredictable crisis, but by collective overconfidence accumulated over years of uninterrupted gains.

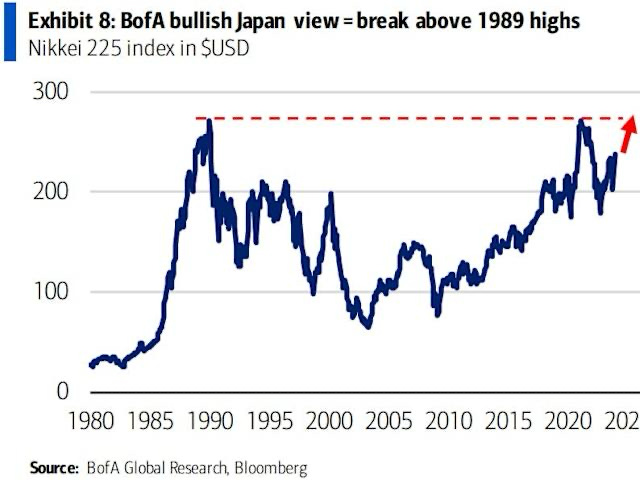

Japan is even more brutal. The Nikkei hit its peak in December 1989 at 38,915 points. It didn’t return to that level until 2024. Thirty-five years. Investors who did everything “right” by the dominant playbook of the era who diversified, who held, who didn’t panic sell and who died with portfolios still underwater relative to their entry point.

These aren’t anecdotes. They are reminders of what happens when consensus is wrong at a real inflection point.

And I believe we’re at one.

The reason I sold equities isn’t macro in the classical sense. It’s not just interest rates, fiscal deficits, or stretched valuations, though all of that compounds. The reason is more specific. And more unsettling.

Corporate guidance is beginning to incorporate, quietly still, the impact of AI on cost structures. And what that guidance will reveal over the coming quarters is that human capital, which represents between 60% and 80% of operating costs for most service companies, is in the process of being replaced.

Not for every company. There will be extraordinary winners. Those that own the models, those that control the infrastructure, those that have built competitive advantages on proprietary data. Those companies can multiply margins in ways the market hasn’t priced yet.

But the vast majority of the index is not those companies.

They are consultancies, mid-sized banks, insurers, retailers, logistics firms, professional services companies. Businesses that for decades built their moat on the cost of replicating their human capital. That moat is disappearing. And the market hasn’t discounted it yet because nobody wants to be the first to leave the party.

When guidance starts including lines like “30% headcount reduction expected for 2026” or “automation of processes equivalent to 500 FTEs,” current multiples will be exposed. And in an environment where the index trades near all-time highs on a cyclically adjusted price-to-earnings basis, there is no margin for error.

My portfolio today looks like this.